Last updated on December 25th, 2024 at 03:57 pm

The Basel Capital Accord is an agreement made in 1988 by representatives of G-10 countries to establish standardized risk-based capital requirements for banks across the globe.

This framework was developed to make financial institutions more resilient in the face of unforeseen events, providing a stable approach to risk management.

What is a Basel Accord?

After the global financial turmoil in 1974, G-10 countries established the Basel Committee on Banking Supervision (BCBS), initially comprising the central bank governors of these countries.

The committee’s main goal was to strengthen financial institutions, making them more capable of handling major risks within the banking sector.

The Basel Accord refers to a set of rules devised by international financial experts to ensure banking stability.

The first version, Basel I, was introduced in 1988, followed by updates in Basel II (2004) and Basel III (2009). While the specifics of each accord have evolved, their core objective remains the same: to protect banks from significant risks.

Basel I (1988)

Basel I set a minimum capital requirement for financial institutions, linking it to the risk of their assets.

In essence, the more risky a bank’s assets (like loans and investments), the more capital it must hold to mitigate potential losses.

Banks were required to maintain a minimum capital equal to 8% of their risk-weighted assets (RWA). These assets were categorized as follows:

- 0%: Low-risk assets (e.g., cash, government bonds).

- 20%: Loans secured by mortgages or high-quality collateral.

- 50%: Loans with moderate security, like residential mortgages.

- 100%: High-risk loans, including non-performing assets (NPAs) or loans to risky debtors.

Additionally, off-balance-sheet items (e.g., derivatives, letters of credit, bank guarantees) were also considered in calculating a bank’s risk-weighted assets.

Basel II (2004)

Basel II was introduced to improve upon Basel I by better addressing financial and operational risks faced by banks.

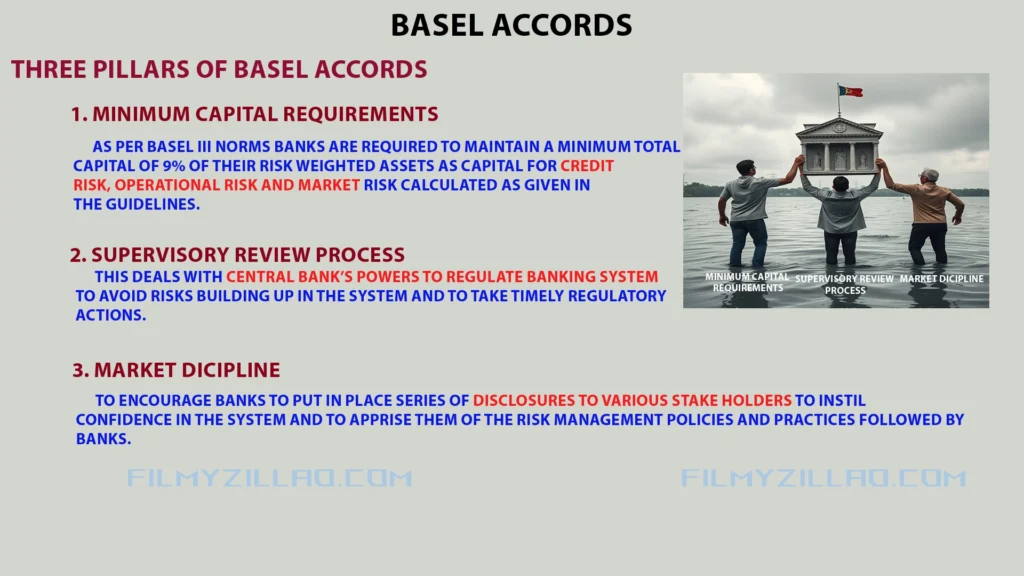

1. Minimum capital requirements

Similar to Basel I, this pillar requires banks to hold capital based on the risks they face, but with a more detailed assessment of risk factors.

2. Supervisory review process

This ensures regulators can effectively oversee and assess banks’ risk management processes and capital adequacy.

It emphasizes the need for a simple, efficient monitoring system.

3. Market Dicipline

Basel II introduced measures to promote transparency. By encouraging banks to disclose critical information regularly, it helps create a market environment that rewards safe banking practices and allows regulators to monitor risks early.

Basel III

Basel III was developed after the 2008 financial crisis, which exposed shortcomings in Basel II. The Basel III includes stricter regulations to strengthen the banking system further.

It builds on the Three Pillars of Basel II and introduces additional measures to address market risk and liquidity risk.

Key changes include:

- Capital Buffers: Banks are required to maintain higher capital reserves to absorb shocks during economic downturns.

- Leverage Ratio: Basel III introduced a non-risk-based leverage ratio to prevent excessive borrowing.

- Liquidity Requirements: New rules ensure banks have enough cash flow to cover short-term obligations, including the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR).

Additionally, Basel III has introduced regulations related to reserve funds like the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR), which are adjusted based on the institution’s financial health.

Importance of Basel Norms

The Basel norms are crucial because they provide a global framework to ensure financial stability and reduce the risk of bank failures.

By setting clear guidelines for capital requirements and risk management, these norms help banks maintain sufficient capital reserves to protect against unexpected losses.

This not only promotes stability in the financial system but also increases the confidence of depositors, investors, and regulators.

Overall, the Basel Accords play a pivotal role in minimizing the risk of financial institution failures, contributing to a more resilient global banking system.